They say that comparison is the thief of joy, but in the banking world, comparison is the bedrock of survival.

Whether you are managing a small community bank with ten employees or steering a multi-billion dollar institution, you are constantly looking at the peer group. You look at their ROA, their efficiency ratios, and their net interest margins. You do this not out of envy, but out of a necessity to understand where the market is moving and ensure you aren’t being left behind in the race for stability and talent.

One of the most significant, yet often under-discussed, benchmarks in this comparison is Bank-Owned Life Insurance (BOLI).

If you’ve spent any time in the C-suite, you know that BOLI is no longer a "niche" strategy. It has become a standard tool for high-performing banks to offset the rising costs of employee benefits. But the question remains: Is your bank above or below the BOLI average? And more importantly, if you are an outlier, do you know why?

The State of the Market: By the Numbers

To understand where you stand, we have to look at the cold, hard data. As we move through 2026, the reliance on Bank-Owned Life Insurance has reached a critical mass.

Currently, 67% of all banks in the United States hold BOLI on their balance sheets. It is the majority position. If you don't have it, you are officially in the minority.

But holding it is only half the story. The depth of the investment is where the strategy really reveals itself. Among those who do hold BOLI, 65% have more than 3.5% of their Tier 1 assets committed to these programs. When we look at the heavy hitters: institutions with over $50 billion in assets: the average BOLI holding jumps to 12.8% of regulatory capital.

Why the disparity? Large institutions didn't get large by accident. They realized long ago that "benefit bleed": the slow, steady drain of capital used to fund executive retirements and rising healthcare costs: is a silent killer of shareholder value. They use BOLI as a specialized asset to recover those costs.

Why Averages Matter (and Why They Don't)

When a CEO asks me, "Matt, are we holding too much BOLI?" I rarely start with a number. I start with a question about their The Perfect Plan®.

Averages are a great starting point for a conversation, but they are a terrible way to run a business. If your bank is currently holding 2% of Tier 1 assets in BOLI while your peers are at 12%, you aren't "safer": you are likely just less efficient. You are paying for benefits with after-tax dollars while your competitors are using tax-advantaged assets to do the heavy lifting.

However, being "above" the average carries its own set of responsibilities. If you are pushing toward that 25% regulatory capital concentration limit, your documentation, your risk assessment, and your board oversight must be bulletproof.

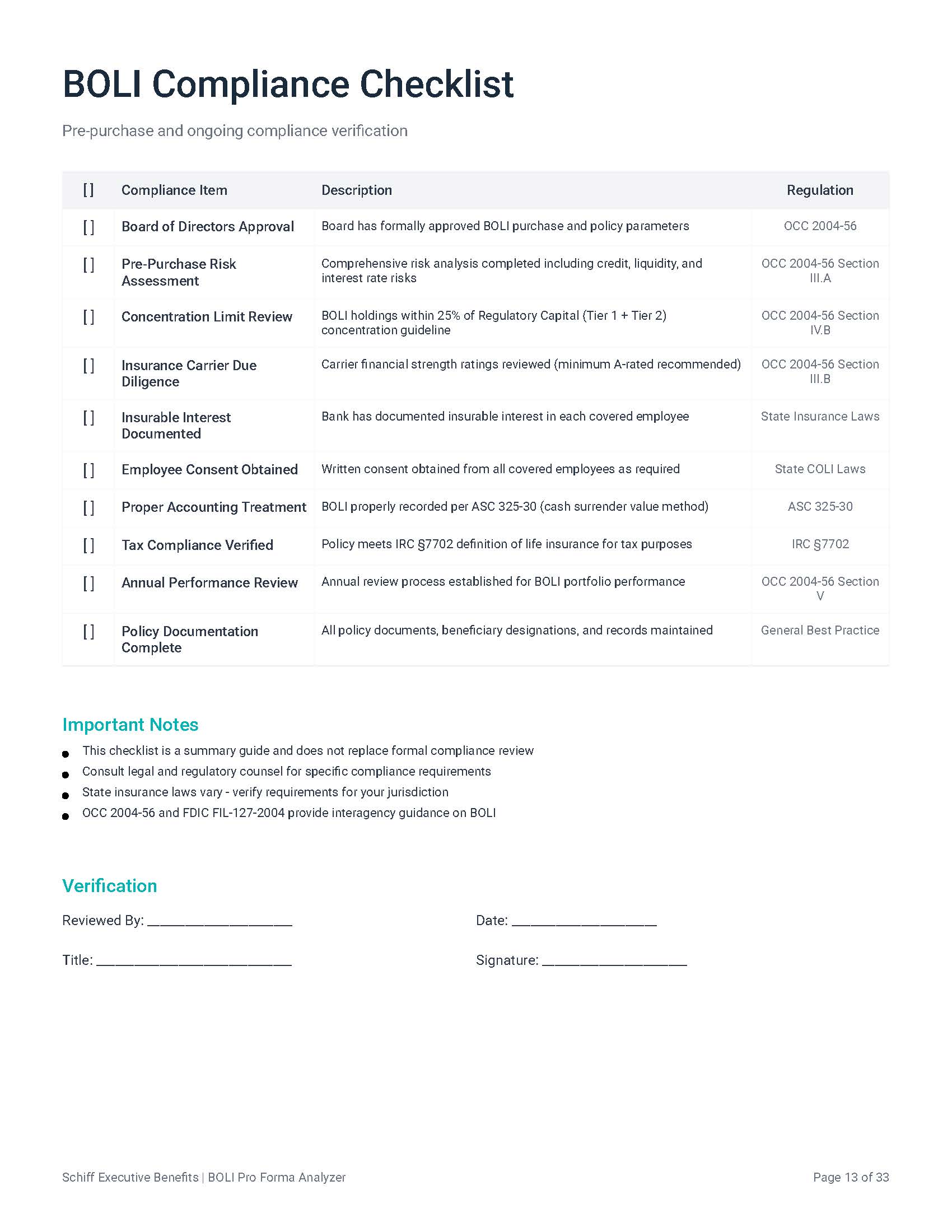

The Technical Guardrails: OCC 2004-56 and IRC 7702

In this environment, you can’t afford to "wing it." The regulatory landscape for BOLI is defined largely by OCC Bulletin 2004-56. This isn't just a suggestion; it's the rulebook. It requires banks to perform comprehensive pre-purchase analysis and ongoing monitoring.

One of the most critical technical aspects we navigate with our clients is IRC Section 7702. This section of the Internal Revenue Code defines what actually constitutes a "life insurance contract" for federal tax purposes. If your policy doesn’t meet these stringent requirements, you lose the very tax advantages: tax-free inside buildup and tax-free death benefits: that make BOLI attractive in the first place.

At Schiff Executive Benefits, we focus on ensuring that every program we design is compliant not just today, but for the long haul. We reverse engineer the solution based on your specific liabilities, ensuring that the asset matches the intent.

Managing the 6 Key Risks

When the regulators come knocking, they aren't just looking at your earnings. They are looking at your risk management framework. OCC 2004-56 outlines six key risks that every bank must address regarding their BOLI holdings:

- Liquidity Risk: BOLI is an illiquid asset. You can't just flip it for cash tomorrow without potential tax penalties and surrender charges. How does this fit into your overall liquidity profile?

- Transaction/Operational Risk: This involves the complexity of the program. Is it being administered correctly? Are the death benefits being tracked?

- Reputation Risk: What happens if the carrier fails? Or if the public perceives the plan as "excessive"?

- Credit Risk: You are essentially making a long-term loan to an insurance carrier. Is that carrier stable? We work as a broker with a wide variety of top-tier carriers to ensure diversification and credit quality.

- Interest Rate Risk: BOLI values can fluctuate based on the interest rate environment. Does your board understand the impact of a rising or falling rate environment on your BOLI yield?

- Compliance/Legal Risk: From insurable interest laws to the 25% concentration limits, the legal hurdles are high.

Offsetting Benefit Bleed: Matching Assets to Liabilities

The most common "What If" we hear from bank presidents is: "What if our top talent leaves for the competitor down the street?"

In the current war for talent, standard 401(k) plans often fall short for high-earning executives due to IRS contribution limits. This is where we implement specialized tools like the 401k Mirror Plan.

But here is the catch: creating a promise (a liability) to pay an executive a SERP (Supplemental Executive Retirement Plan) or a Mirror Plan benefit in 15 years is easy. Funding it is the hard part. If you don't have an asset earmarked to grow alongside that liability, you are creating a massive hole in your future balance sheet.

By utilizing BOLI, we can match the asset to the future liability. When the executive retires, the cash value of the BOLI can provide the cash flow to pay the benefit. If the executive passes away prematurely, the death benefit protects the bank and the executive's family. It’s about restoring alignment and retention.

The Schiff Approach: Reverse Engineering Your Success

We don't believe in "off-the-shelf" products. Our team has almost 100 years of combined experience in technical benefit design. We don’t start with a BOLI policy; we start with your goals.

We ask the tough questions:

- What is the cost of your current benefit "bleed"?

- How much of your capital is working for you versus sitting in low-yield traditional assets?

- Are your top three executives truly tied to the long-term success of the bank?

Once we have those answers, we "reverse engineer" a solution that fits your culture. We call this The Perfect Plan®. It’s a process that ensures your benefits are a bridge to your goals, not a weight on your earnings.

Where Do You Go From Here?

If you find that your bank is below the average, don't panic. It’s an opportunity. It means you have "eligible purchase capacity": dry powder that can be deployed to increase your ROA and secure your key people.

If you are above the average, it's time for a check-up. Are you managing those six key risks? Is your documentation up to the standards of the latest OCC exams?

Regardless of where you sit on the curve, the goal is the same: realizing your dream value and building it your way. Don't let your executive benefits be an afterthought.

If you want to see exactly how your bank stacks up against a specific peer group: not just national averages, but the banks in your own backyard: let’s talk. Sit back, grab your coffee, and come join us for a deeper dive into the technical side of retention.

Your legacy is too important to leave to chance. Let's make sure you have The Perfect Plan® in place and help your bank maximize your BOLI Portfolio. Our Proprietary BOLI Model can give you a peer analysis and projected earnings analysis in seconds. Give us a call at 610-292-9330 or email us at info@schiffbenefits.com for your bank's copy. We're here to help, and have the expertise to work with ANY carrier.

Learn more: our complete guide to Bank Owned Life Insurance (BOLI).

They say that the only constant in life is change, but in the world of high-stakes banking and executive leadership, the only constant is the relentless need for top-tier talent. Without the right people in the right seats, even the most storied financial institutions are just buildings with impressive vaults.

They say that the only constant in life is change, but in the world of high-stakes banking and executive leadership, the only constant is the relentless need for top-tier talent. Without the right people in the right seats, even the most storied financial institutions are just buildings with impressive vaults.