The only constant in the world of high-stakes business is change, yet one truth remains universal: your business is only as strong as the people who lead it. For decades, the most successful organizations have understood that attracting and retaining top-tier talent isn't just about a competitive salary: it’s about creating a sense of ownership and securing a legacy.

But as you scale, the tools you use to build that security become increasingly complex. You move from simple "handshakes" to sophisticated financial structures. Among these, few are as powerful: or as misunderstood: as Split Dollar life insurance. When built correctly, it is a masterpiece of financial engineering. When built poorly, it can trigger a regulatory nightmare.

At Schiff Executive Benefits, we specialize in reverse-engineering these solutions to ensure they match your company culture and intent while "Restoring Alignment and Retention." To navigate this landscape, you need to understand the "architecture" of the plan: the interaction between tax regimes, the impact of the Sarbanes-Oxley Act (SOX), and the technical nuances of Internal Revenue Code (IRC) Section 409A.

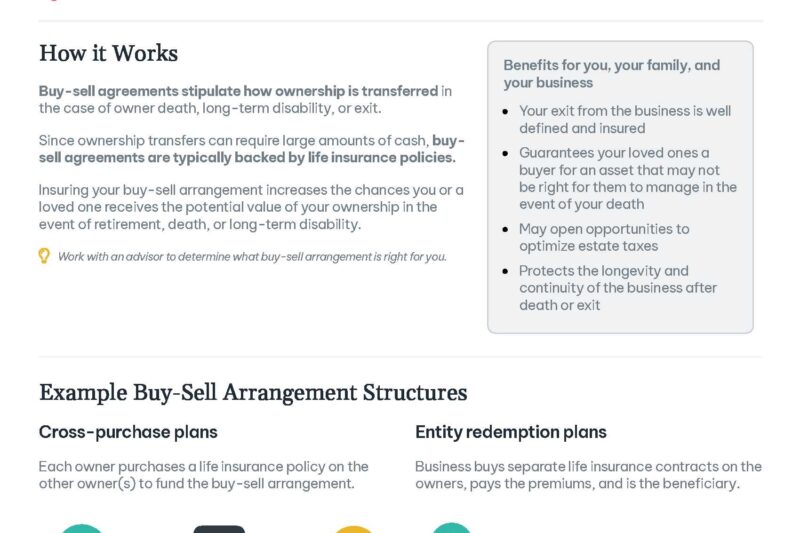

The Two Foundations: Collateral Assignment vs. Endorsement

Think of a Split Dollar arrangement as a partnership between an employer and a key executive to share the costs and benefits of a life insurance policy. However, the way you structure that partnership determines everything from who owns the policy to how the IRS views the transaction.

1. The Loan Regime (Collateral Assignment)

In a Collateral Assignment Split Dollar (CASD) arrangement, the executive owns the policy. The employer pays the premiums, but those payments are treated as a series of loans to the executive. To secure the repayment of these loans, the executive assigns the policy’s cash value or death benefit to the employer as collateral.

This is often the preferred route for private companies because it allows for a more efficient transfer of wealth. However, because it is technically a loan, it must follow the rules of IRC Section 7872, requiring a market-rate interest or the imputation of income to the executive.

2. The Economic Benefit Regime (Endorsement)

In an Endorsement Split Dollar arrangement, the employer owns the policy. The employer "endorses" a portion of the death benefit to the executive’s beneficiaries. Here, the executive is not receiving a loan; they are receiving a taxable "economic benefit" (the value of the current life insurance protection).

While this is simpler from a documentation standpoint, it is often less flexible for long-term retirement planning than the loan-regime approach.

The SOX 402 Hurdle: A Warning for Public Companies

If you are a decision-maker at a public company (or a company planning to go public), the architecture of your Split Dollar plan faces a significant regulatory roadblock: Section 402 of the Sarbanes-Oxley Act.

Passed in the wake of major corporate scandals, SOX Section 402 made it unlawful for any public issuer to extend or maintain credit in the form of a "personal loan" to any director or executive officer. Because a Collateral Assignment Split Dollar plan is legally structured as a loan, it falls squarely into the crosshairs of this prohibition.

For the top five employees in a public company, the loan-regime approach is generally a "no-go." Implementing a CASD plan for these individuals could lead to severe legal and civil penalties. In these environments, we typically pivot toward Endorsement structures or other Non-Qualified Deferred Compensation (NQDC) models that avoid the "loan" definition entirely.

409A and the Strategic Loan: Planning for the "What If"

One of the most attractive features of a Split Dollar loan is the possibility of loan forgiveness. Imagine a scenario where, after 15 years of exceptional service, the company forgives the executive's debt, effectively turning the life insurance policy into a tax-efficient retirement windfall.

However, if you don't plan for this from the start, you are walking into a trap set by IRC Section 409A.

Section 409A governs nonqualified deferred compensation. If a company decides on a whim to forgive a Split Dollar loan at retirement, the IRS may view that forgiveness as a "deferral of compensation." If the arrangement wasn't drafted to comply with 409A from day one, the executive could face immediate income inclusion, a 20% penalty tax, and premium interest charges.

"In the Room Where It Happened"

This is where technical expertise becomes your greatest asset. Our President, Matt Schiff, doesn't just read these laws; he was "in the room" when they were being shaped. In 2003 and 2005, Matt served as a ranking member of the AALU’s NQDC Committee alongside Michael Goldstein. Together, they helped draft the very laws: IRC 409A and 101(j): that govern these plans today.

When we talk about "Split Dollar Architecture," we aren't just following a template. We are using the same deep technical insight that helped establish the regulatory framework.

The History of Deferred Compensation

To truly understand why these rules exist, it helps to look back at the history of the industry. We recently sat down with Dan Hogans, formerly of the IRS Treasury and one of the primary architects of the 409A regulations, to discuss how we got here.

You can watch that full conversation, "The History of Deferred Compensation," on The Perfect Plan® Podcast. It’s a masterclass in how regulatory shifts changed the way businesses protect their key people.

At Schiff Executive Benefits, we integrate these lessons into every Perfect Plan® we design. Whether it's ensuring 100% protection for employee families or creating a 100% income stream in retirement, the goal is always the same: security through precision.

Why "Reverse Engineering" Matters

Most brokers start with a product. They have a policy they want to sell, and they try to fit your company into it. We take the opposite approach. We reverse-engineer the solution based on your specific goals.

- Are you a public company? We avoid the SOX 402 traps.

- Are you a private firm looking for a "Golden Handshake"? We structure the CASD with 409A-compliant forgiveness triggers.

- Are you worried about cost recovery? We design the Cost Recovery Engine to ensure the business eventually receives every dollar it put into the plan.

We work as an integrated part of your advisory team, collaborating with your accountants and attorneys to ensure that the plan we build today doesn't become a liability tomorrow.

Realizing Your Dream Value

Your business is your legacy. The people who help you build it deserve a plan that is as robust and well-thought-out as the company itself.

Are you asking the right "What If" questions?

- What if your top talent leaves for a competitor tomorrow?

- What if a senior executive retires and the replacement cost exceeds your budget?

- What if you could provide "Ownership Feel" to non-owners without giving away equity?

The answers to these questions lie in the architecture of your benefits. By utilizing The Perfect Plan®, you aren't just buying insurance; you are implementing a strategic retention tool that scales with your success.

Come Join Us

Navigating SOX, 409A, and Split Dollar regimes can feel like walking through a minefield. But you don't have to do it alone. Sit back, grab your coffee, and let’s look at how we can reinforce your company's foundation.

Whether you are a small business with 10 employees or a large corporation with 10,000, the principles of retention and alignment remain the same.

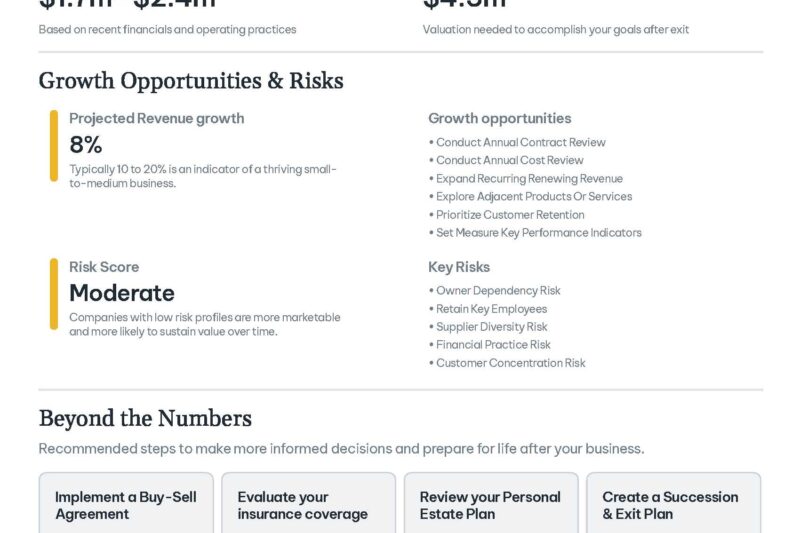

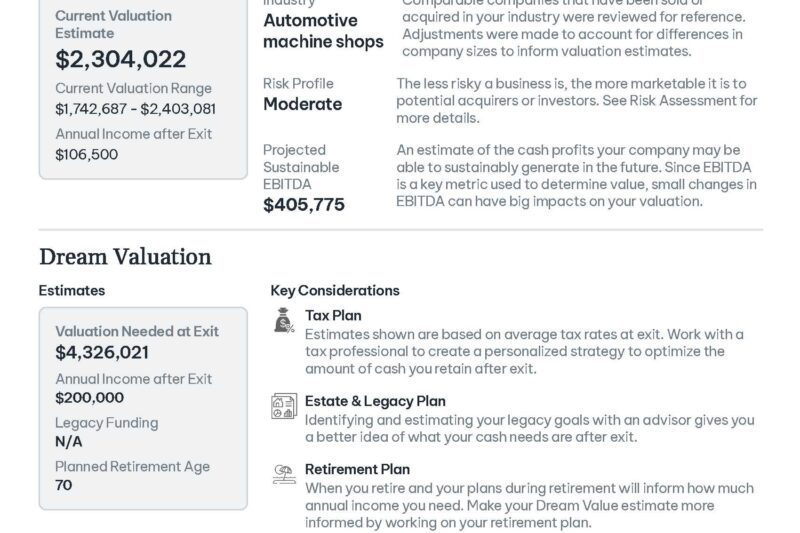

Ready to see what your business is truly worth and how you can protect it?

Get your professional business valuation here using the RISR tool.

Let’s build something that lasts.

They say that the only constant in life is change, but in the world of high-stakes banking and executive leadership, the only constant is the relentless need for top-tier talent. Without the right people in the right seats, even the most storied financial institutions are just buildings with impressive vaults.

They say that the only constant in life is change, but in the world of high-stakes banking and executive leadership, the only constant is the relentless need for top-tier talent. Without the right people in the right seats, even the most storied financial institutions are just buildings with impressive vaults.