In this episode of the Perfect Plan™ podcast, Matt welcomes welcome Holland Haiis as our special guest! Holland is a renowned workplace strategist, speaker, and author who helps individuals and organizations boost productivity, improve communication, and unlock human potential. Known as the "Digital Detox Coach," Holland empowers people to thrive by balancing the digital demands of today's world with intentional human connection. In this episode, Holland and Matt dive deep into creating a Perfect Plan™ for leadership, communication, and living a more connected life — both online and offline. Trust me, this conversation is packed with insights you can apply right away!

Learn More About Holland: https://www.hollandhaiis.com/

If you are a business owner or decision making executive, how would you want to design The Perfect Plan™ to retain and reward your employees? A 401K is terrific for basic retirement savings, but there are limitations to how much you can put in, and it must be given to everyone on a proportional basis.

In this episode, we discuss the decision making process, how you can get the perfect timing of your deductions, and include the people and benefits that are needed most, in the most tax efficient manner. No two companies are alike, and neither should your plans be.

Come and listen to this podcast as we lay it out for you.

Every business owner starts their business with the intent to "sell it" sometime in the future, make a lump sum, and walk away. Most likely, if you are reading this, you're more than far enough along in your ownership journey that you are now asking yourself:

"How much is my business worth?".

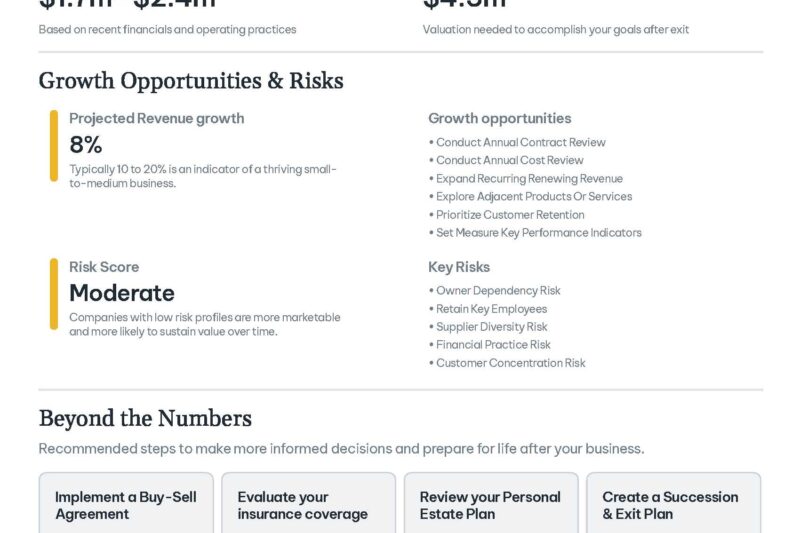

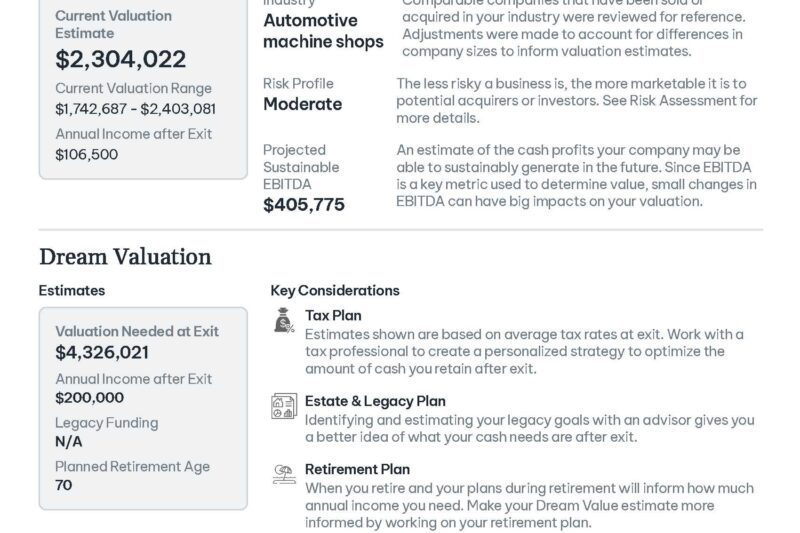

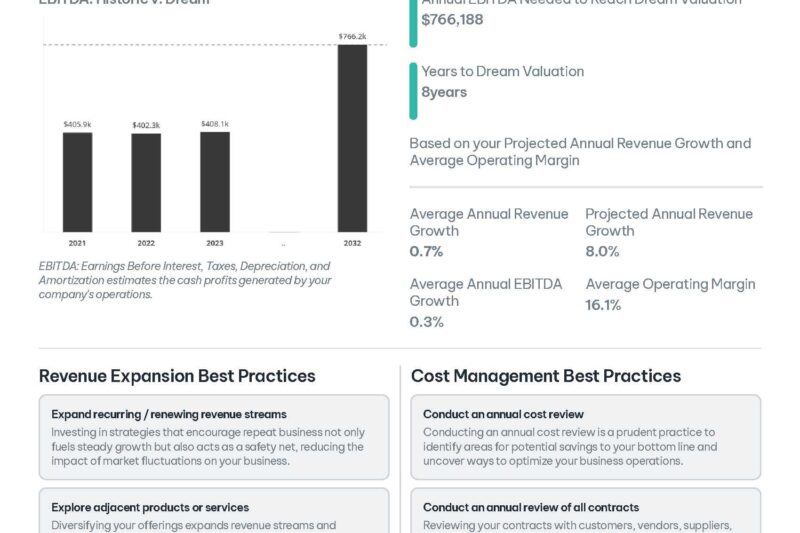

At Schiff Executive Benefits (SEB), we use a business valuation program called RISR that can help you find out. If you use Quickbooks, an owner can share their last three years of tax related data electronically, seamlessly, and securely through a link that we will send you to your PRIVATE valuation. After uploading that data, and answering a few questions about the operation of the business (i.e. ownership, tax structure, client concentration, operational questions, etc.), RISR will generate a SNAPSHOT value for SEB to review with you, so that you can realize your DREAM value in the future.

Using the results from the report, you can:

- Negotiate offers with potential buyers,

- Discuss with management ways to improve profitability

- Review potential business valuation risks, and

- Align your people with the future growth of the company.

Here were some of the solutions that our clients decided upon after engaging SEB:

- Sold to an outside party

- Implemented an Installment (structured) sale to the employees/family member

- Employee Stock Ownership Plans

- Sell some or ALL of your stock

- Retain Control of the company

- Immediate Tax Savings for an S Corp

- Provides Retention Strategy for ALL employees

- Buy/Sell Planning Between Partners upon:

- Death

- Disability, or

- Retirement

- Tax Efficient Retention Strategies

- Executive Bonus

- Restricted Executive Bonus (REBA)

- Supplemental Retirement Plan

- Excess 401K Plans

- For YOUR report specific to YOUR company, Complete the form below to request your link for your business valuation.

A FULL sample report can be downloaded here: Schiff Auto report

In a PERFECT world, how would you design a "benefit" plan for you (the Business Owner), your key executives, and your family? Well, in this Episode, Matt goes through some design options available when starting a brand new plan. In essence, you have a blank piece of paper that allows you to build it YOUR way.

Sit back grab your coffee, and listen to some options available to you depending on your role.

https://youtu.be/VUsv8NaXsrc

Are you a business owner? Have you ever thought about selling your business? How much is it worth? Do you have other shareholders, or family that own part of the business?

Well, in this, the Sixth episode of The Perfect Plan, Dan Zugell, my friend and colleague of 25 plus years goes into the wonder of an Employee Stock Ownership Plan (ESOP). In this qualified retirement plan solution for a business owner, you have a ready and willing buyer, that will buy your business, for a set dollar amount, at a set triggering event. If done correctly, you as the business owner can still run it, control it, and participate in the future growth of your company.

Dan goes into the benefits, tax advantages, and rules of how to design "the perfect" exit strategy for the closely held business owner. Take a few minutes and hear what he has to say, then contact us on how we can help you monetize your largest asset.

Ps. You can schedule a direct call with Dan at https://dantheesopman.com/ or with SEB at Calendly - Matthew E Schiff

As a business owner, how do you keep your best people and properly plan for yourself and your executives? Well, Bud Schiff, past President of Mutual of New York (MONY), past president of NYLEX Benefits, managing director of Alvarez and Marsal gives his insight of over 50 years in this podcast about employee retention strategies.

If you want to find a way to "retain" your best employees in a post no "non-compete" environment, listen up, and then give us a call. It's easier than you think, and it costs more to retrain a new hire, than it is to retain your best employee.

Are you an Attorney, Accountant, TPA, Trust Officer, Insurance Agent, Property and Casualty agent? If you work with Business Owners, and their families, then you want to be at this meeting where you will hear about how to COLLABERATE with other professionals who work with your client.

We will spend the day on Thursday, May 16th at the Fitler's Club in Philadelphia sharing a case study that is VERY relevant in today's world. How do you handle the intricacies of the family while bringing together all needed advisors to work seamlessly?

Well, we will have 20-25 attendees from different professions, coming together to discuss the challenges that they are facing with their clients in 2024. Come join us, and network with some of the best in their fields.

P.S. The night before, we have a Box at Citizens Bank Park for the game between the NY Mets and the Philadelphia Phillies (@6:40pm).

Sign up below to save your spot.

Check out the Latest Trends in Executive Benefits in the latest Schiff Executive Benefits (SEB) Newsletter. This month, learn:

- How to "monetize" your business while still controlling it (ESOP)

- How to retain key employees with a deductible benefit that has a risk of forfeiture

- Implement a Long Term Benefit on a Company wide Basis (with little to no underwriting)

Actionable Ideas to Recruit, Retain

and Reward Key Talent

In a time when more executives are walking away from their jobs, what can you do to keep them leaving during the Great Talent Recognition? Well, in this article by Andreas Stuermann, a fellow Lion Street Owner, he shares his ideas and insight into what might interest you and your staff that isn't for everyone, discretionary, and may be fully cost recvoered.