A business is only as strong as the promises it keeps to its key people. In the world of high-growth, mid-cap companies: the "stocks under rocks" often highlighted in the Burkenroad Reports: talent is the primary engine of value. When we look at companies like Pool Corp (POOL), Haverty Furniture (HVT), Powell Industries (POWL), and Cal-Maine Foods (CALM), or financial institutions like First Bancshares (FBMS) and First Guaranty Bancshares (FGBI), we see organizations that have built incredible legacies.

But here is the universal truth: Your most valuable assets walk out the door every night. Whether they come back the next morning: and whether they stay for the next decade: depends on more than just a competitive salary. It depends on "Benefit Security."

At Schiff Executive Benefits, we specialize in Restoring Alignment and Retention. We’ve analyzed the public structures of these Burkenroad-profile companies to identify where executive benefits are performing at a high level and where "Operational Drift" might be putting the company: and the executive: at risk.

The "What If" That Keeps Presidents Up at Night

When I sit down with a President or a CEO, I often start with one of our core "What If" questions: What if your top talent leaves?

Think about the replacement cost. It’s not just the recruiter fee. It’s the lost institutional knowledge, the client relationships that follow the executive, and the momentum that stalls during a transition. For companies in the Burkenroad universe, where lean management teams often drive outsized results, the departure of a key leader isn't just a hurdle: it’s a headwind.

The solution isn't simply "more pay." It is about creating an Ownership Feel for those who don’t actually own shares, and providing a level of security that makes it impossible for them to look elsewhere.

Creating an "Ownership Feel" for Non-Owners

For corporations like Powell Industries or Cal-Maine Foods, retaining key managers requires a strategy that mirrors the rewards of ownership without the dilution of equity. This is where Phantom Stock or sophisticated Non-Qualified Deferred Compensation (NQDC) plans come into play.

By structuring a plan that tracks company performance or specific growth metrics, you give the executive a stake in the outcome. They begin to think like an owner because their long-term wealth is tied to the firm’s trajectory. However, a plan on paper is only as good as the funding behind it.

Many companies fall into the trap of "unfunded liabilities." They promise a benefit 15 years down the road but leave the bill for a future management team to pay. This creates a lack of security for the executive. They find themselves asking: Will the money actually be there when I’m ready to exit?

Benefit Security and the Power of Full Cost Recovery

This is where the conversation shifts from a human resources discussion to a balance sheet discussion. For the companies we’ve analyzed, such as First Bancshares and First Guaranty Bancshares, the use of Bank-Owned Life Insurance (BOLI) is a standard tool. For our corporate friends like Pool Corp and Haverty Furniture, the equivalent is Corporate-Owned Life Insurance (COLI).

The goal is Full Cost Recovery.

Most benefit plans are an expense. We view them as a strategic reallocation of assets. By using COLI or BOLI as an informal funding vehicle, the employer can recover:

- The original premium paid into the plan.

- The cost of the benefits paid to the executive.

- The "opportunity cost" of the money (the interest the company could have earned elsewhere).

When structured correctly, the plan becomes "cost-neutral" or even "cost-positive" to the corporation while providing 100% protection to the employee's family and 100% of the promised income in retirement.

Retirement Made Simple: The Four Pillars

In my experience, executive benefit plans often become overly complex, leading to confusion and, ultimately, a lack of perceived value. We advocate for Retirement Made Simple. If an executive at Haverty’s or Powell Industries can’t explain their retirement plan to their spouse in two minutes, the plan is failing as a retention tool.

The Perfect Plan® (as we call our optimized approach) focuses on four fixed pillars:

- Fixed Dollar Amount: The executive knows exactly what they will receive.

- Fixed Period: The duration of the payments is defined and guaranteed.

- Fixed Rate of Return: No market volatility keeping the retiree awake at night.

- Fixed Cash Flow: A predictable stream of income that supplements the 401(k) limits.

When you offer "Retirement Made Simple," you remove the anxiety of "running out of money," which is one of our primary "What If" anchors. You can learn more about how we frame these outcomes by visiting our The Perfect Plan®.

Technical Compliance: Avoiding "Operational Drift"

One of the biggest risks we see in the Burkenroad companies is Operational Drift. A plan that was compliant and efficient in 2010 may be a ticking time bomb today due to changes in IRC 409A and IRC 101(j).

IRC 409A: The Safe Harbor Update

IRC 409A governs how and when deferred compensation is paid. The penalties for non-compliance are draconian: immediate taxation of all deferred amounts plus a 20% penalty tax on the employee. We often find that companies haven't updated their "Safe Harbor" language to reflect modern IRS guidance. If you haven't audited your NQDC plan in the last three years, you are likely drifting. You can watch a short overview of 409A compliance here.

IRC 101(j): The Notice and Consent Rule

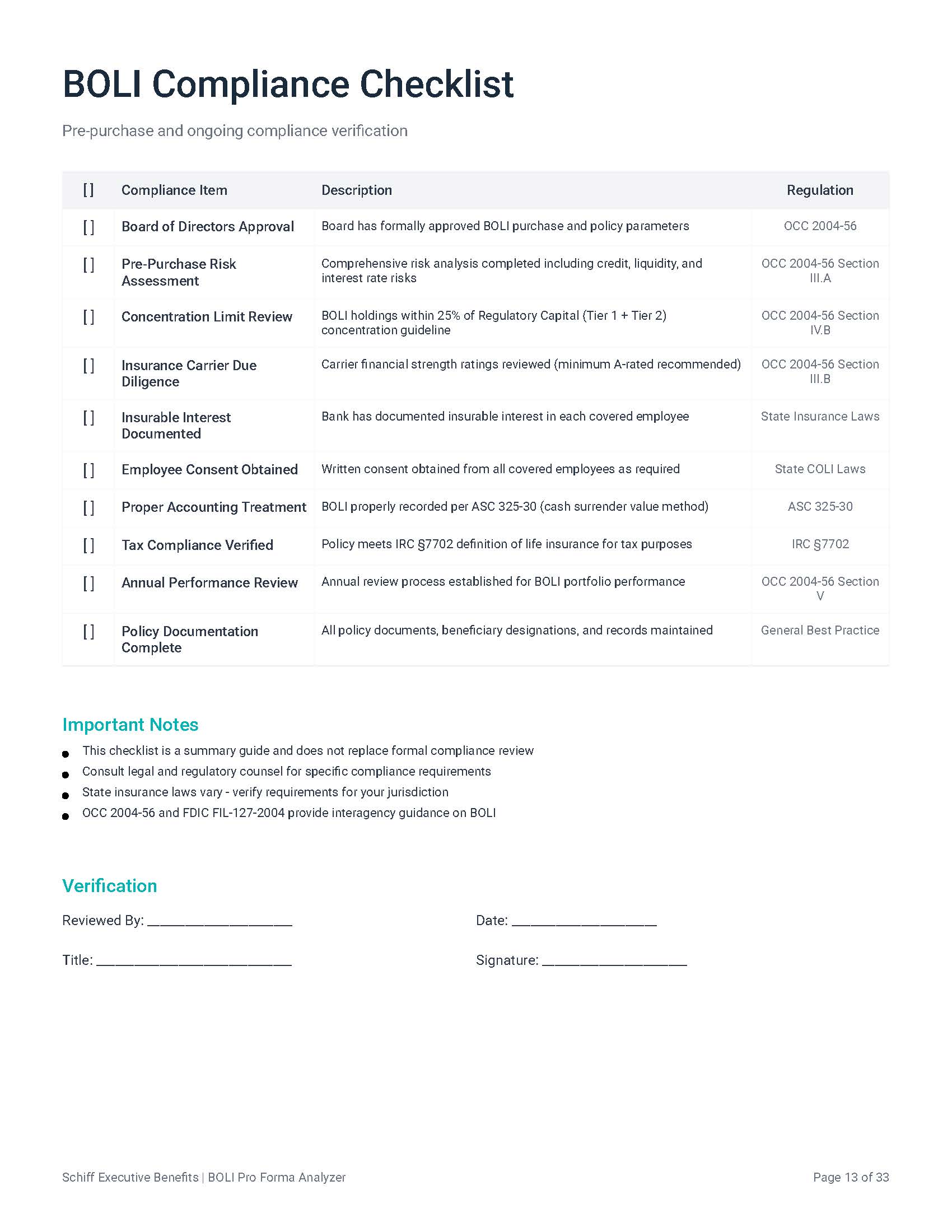

For companies using COLI (Corporate-Owned Life Insurance) to fund these plans, compliance with IRC 101(j) is non-negotiable. If you do not obtain written consent from the executive before the policy is issued, the death benefit: which is supposed to be tax-free: becomes taxable income to the corporation.

Benchmarking the Burkenroad Peer Groups

When we look at the specific companies in this analysis, we see a range of maturity in their executive benefit structures.

- Financial Institutions (FBMS, FGBI): These banks generally understand BOLI but often lack a post-purchase analysis to ensure their peer group benchmarking is up to date. Are you holding too much cash in the plan? Is your BOLI/Capital ratio optimized?

- Retail and Industrial (POOL, HVT, POWL, CALM): These corporations often have "Legacy Plans" that are either under-funded or using outdated insurance products that don't offer the flexibility required for today’s executive.

The question isn't just "Do you have a plan?" The question is "Is your plan still doing its job?"

Restoring Alignment

The goal of any executive benefit strategy should be to align the interests of the shareholder, the company, and the key executive. When an executive at a company like Cal-Maine Foods knows that their family is 100% protected and their retirement is 100% secure, their focus remains on driving the business forward.

They aren't looking at the "next big offer" because they are already participating in The Perfect Plan®.

If you are a Center of Influence (COI) advising these companies, or an executive within one of these organizations, it’s time to move past the "set it and forget it" mentality. The economic environment has shifted, and your retention strategies must shift with it.

We invite you to retain your key people with ownership-like benefits and ensure your organization is protected against the "What Ifs" that matter most.

Sit back, grab your coffee, and let’s look at your plan together. We’re here to act as your guide through the complexities of executive security, ensuring your legacy: and the legacies of your top talent: are built on a foundation that lasts.

Come join us for Part 2, where we will dive deeper into the specific financial impact of "Full Cost Recovery" for the Burkenroad industrial sector.

Matt Schiff

President, Schiff Executive Benefits

Restoring Alignment and Retention

Learn more: executive retention programs.