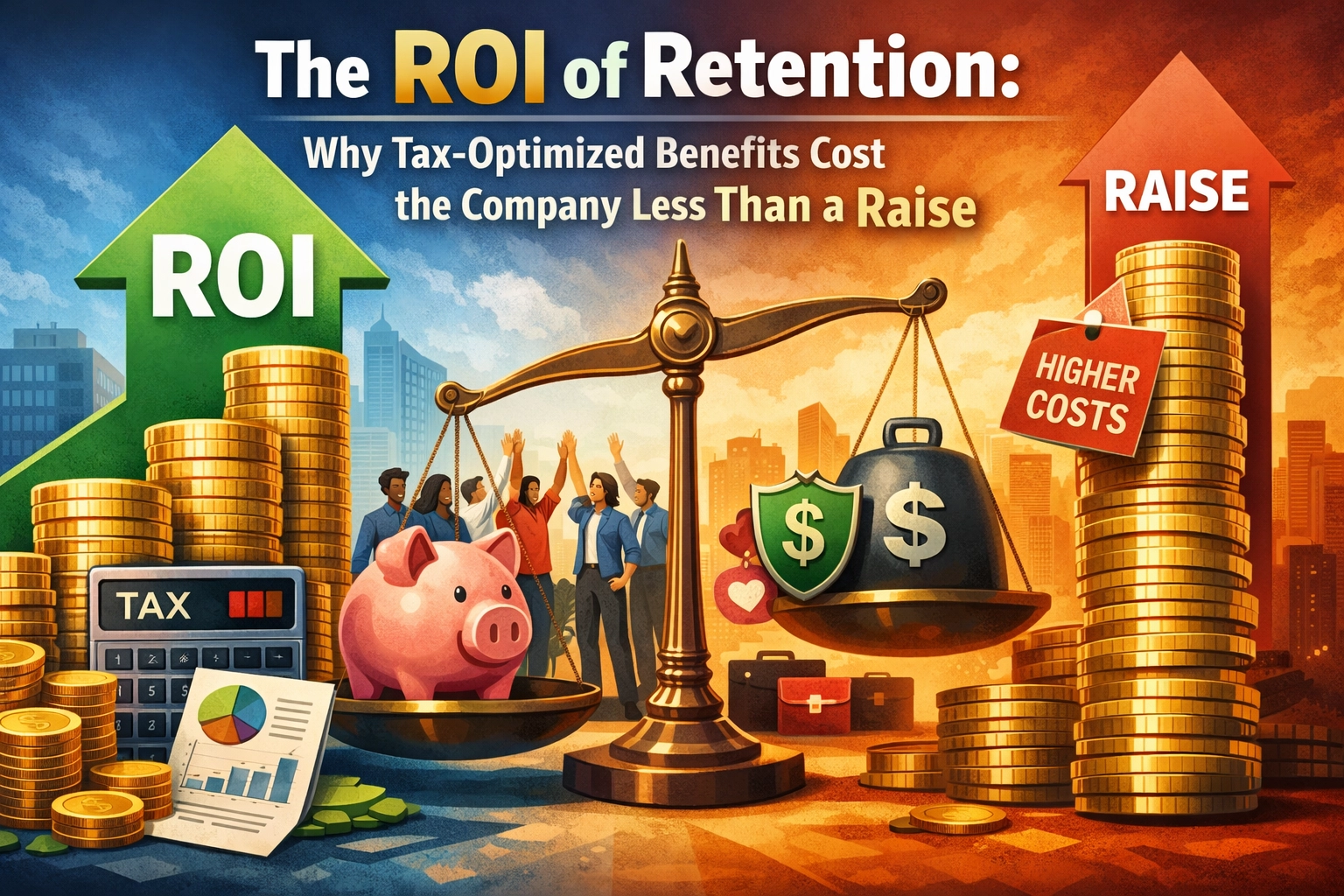

In business, it is an undeniable truth that it isn’t what you make: it’s what you keep. This principle applies to your personal wealth, your company’s bottom line, and, perhaps most importantly, your key employees’ take-home pay.

Every business owner has felt the sting of the "Retention Hamster Wheel." You have a superstar: someone who knows your systems, your clients, and where the bodies are buried. They come to you with a job offer from a competitor for 15% more than their current salary. You want to keep them, so you match it. But here is the problem: to give that employee a $20,000 raise, it actually costs your company significantly more than $20,000, and the employee sees significantly less than $20,000 after the IRS takes its cut.

Are you simply funding the government’s coffers while trying to save your own culture? There is a better way.

The Friction of the Traditional Raise

When you increase a key executive’s salary, you are choosing the least tax-efficient way to move capital from the business to the individual. First, the company pays payroll taxes on that increase. Then, the employee pays ordinary income tax: often at the highest marginal rate: plus state and local taxes. By the time that "raise" hits their bank account, it has been eroded by 40% or more.

Worse yet, a raise offers very little in the way of "Golden Handcuffs." Once a salary is increased, it becomes the new baseline. It doesn’t necessarily incentivize the employee to stay for the next five or ten years; it just makes them more expensive today.

What if you could provide a benefit that feels more valuable to the employee, costs the company less in the long run, and creates a powerful incentive for them to stay until retirement?

Enter Tax-Optimized Executive Benefits

At Schiff Executive Benefits, we focus on moving away from "tax-heavy" compensation and toward "tax-optimized" wealth building. By using specialized structures, we can bypass the limitations of traditional 401(k) plans and create meaningful value for your inner circle.

1. Non-Qualified Deferred Compensation (NQDC)

Think of an NQDC plan as a "401(k) Mirror." For your highest earners, the standard IRS contribution limits are often a drop in the bucket. An NQDC plan allows them to defer a much larger portion of their compensation, pre-tax, into a plan where it can grow tax-deferred. For the company, this creates a liability on the books, but one that is tied to the employee’s continued service.

2. Phantom Stock Plans

You want your key people to think like owners, but you don't necessarily want to dilute your actual equity. Phantom Stock mimics the appreciation of your company's value. When the company hits certain milestones or the employee reaches a specific tenure, they receive a cash bonus equivalent to the "value" of the shares. It aligns their interests with yours without the legal headaches of actual stock transfers.

3. Split-Dollar Life Insurance

This is perhaps the ultimate "win-win." The company pays the premiums on a life insurance policy for the executive. The executive gets a massive death benefit for their family and, eventually, access to tax-free cash flow from the policy’s cash value. The company, meanwhile, is eventually reimbursed for every cent it paid in premiums.

The Full Cost Recovery Model: The Business Owner’s Secret

The biggest difference between a "raise" and a "benefit" is what happens to the money after it leaves your hand. When you pay a salary, that money is gone forever. It is a pure expense.

However, many of the strategies we design for our clients utilize the Full Cost Recovery model. By using Corporate Owned Life Insurance (COLI) as the informal funding vehicle for these benefits, the business can actually recover the cost of the program.

Here is how it works:

- The company establishes an executive benefit (like an NQDC).

- The company purchases a life insurance policy on the executive to fund that future liability.

- As the policy grows, it provides the liquidity to pay the benefit.

- Upon the executive’s eventual passing (even long after retirement), the death benefit is paid to the company tax-free, reimbursing the business for the premiums paid and the benefits distributed.

In this scenario, the "cost" of the benefit isn’t the cash outlay: it’s the opportunity cost of the money. Compare that to a salary increase, which is an absolute loss of capital. When you look at the math, tax-optimized benefits don't just cost less; they can eventually become cost-neutral.

The ROI of Peace of Mind

Financial stress is a silent killer of productivity. Research suggests that financial anxiety costs American employers billions annually in lost focus and engagement. By providing your key talent with a structured path to wealth that isn't eroded by immediate taxation, you aren't just giving them money: you're giving them security.

When an executive knows their retirement is secure and their family is protected through a customized executive benefit solution, they aren't looking for the exit. They are looking at how to help you grow the business.

Does your current compensation strategy feel like a sieve, where capital is constantly leaking out to the IRS? Are you worried that your best people are one headhunter call away from leaving?

Building Your Perfect Plan®

We live in an era of economic uncertainty. With national debt rising and tax laws in a constant state of flux, relying on "the way we’ve always done it" is a recipe for stagnation. You need a team of advisors who understand the technical nuances of the tax code and the human nuances of your business culture.

At Schiff Executive Benefits, we don't believe in off-the-shelf products. We believe in The Perfect Plan®: a methodology designed to align your corporate goals with the personal financial needs of your leadership team.

Whether you are looking to protect your business through a modernized buy/sell agreement or you want to ensure your top performers never have a reason to leave, the strategy must be tax-efficient to be effective.

Take the Next Step

You’ve worked too hard to build your business to let tax inefficiency and talent turnover hold you back. It’s time to stop overpaying for "raises" that don't produce a return and start investing in benefits that build long-term value.

Let’s look at the math together. We can help you analyze your current payroll and benefit structure to see where the leaks are and how to plug them.

Schedule a consultation with Matt Schiff via our Calendly link here to discuss how we can implement a tax-optimized retention strategy for your company. Grab a coffee, sit back, and let’s talk about how to protect your legacy and your people.

Want to hear more about these strategies in action? Check out The Perfect Plan® Podcast where we dive deep into the technical and emotional aspects of executive wealth and business succession.