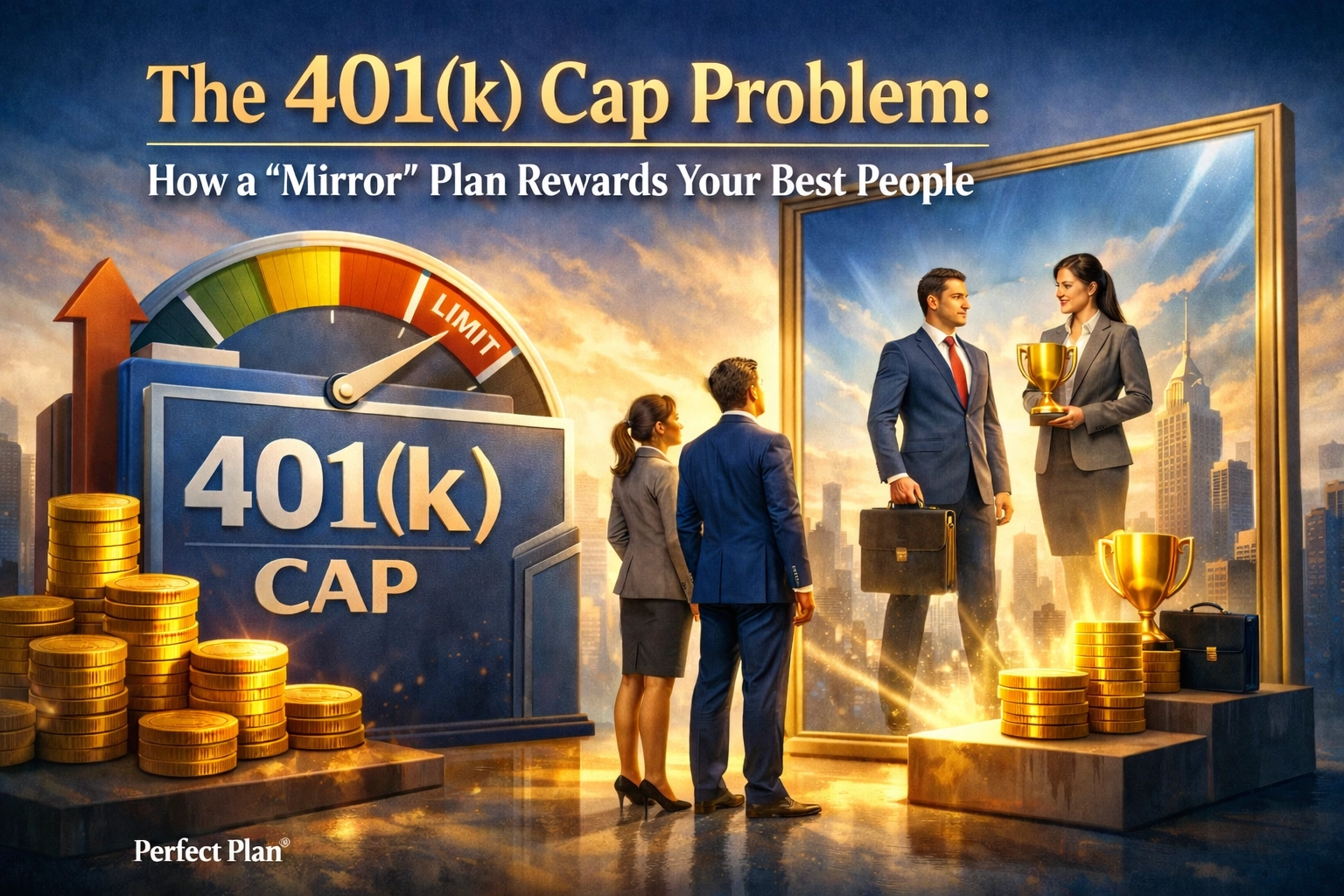

Success in business is often measured by the height of the ceiling you’ve built, but for your top-tier executives, the federal government has installed a ceiling of its own, and it’s remarkably low.

It’s an undeniable truth in the American tax code: the more you earn, the less you are allowed to save for retirement on a tax-advantaged basis, at least proportionally.

While your entry-level employees can comfortably defer 10% or 15% of their salary into a standard 401(k), your President, CFO, or top-performing VP often finds themselves hitting a hard wall.

By the time the high-earners reach the annual IRS contribution limit, they might only be deferring 3% or 5% of their total compensation. Is that fair? Of course not. Is it a risk to your business? Absolutely.

When your vital few, the people who actually move the needle, realize their path to a comfortable retirement is being throttled by outdated IRS caps, they start looking for the exit. They start looking for a company that understands how to reward performance without the handcuffs of qualified plan limits.

The "Reverse Robin Hood" Effect

We’ve all heard the stories of taking from the rich to give to the poor, but the standard 401(k) model essentially creates a "Reverse Robin Hood" scenario. Because of non-discrimination testing and strict IRS contribution limits, your most valuable people are actually the most penalized.

Think about it. If you have a key executive making $350,000 a year, the standard 401(k) limit (currently hovering around $23,000–$30,000 depending on age and catch-ups) represents a tiny fraction of their income. To maintain their lifestyle in retirement, they need to save significantly more. But the "qualified" plan, the one you offer to everyone from the mailroom to the boardroom, simply won't let them.

What keeps you up at night? Is it the fear that your competitors will poach your head of sales with a better "wealth creation" package? If you are only offering a standard 401(k), you are leaving the door wide open for them to leave.

Enter the 'Mirror' Plan: Breaking the IRS Ceiling

At Schiff Executive Benefits, we specialize in what we call The Perfect Plan®. One of the most powerful tools in that arsenal is the Nonqualified Deferred Compensation (NQDC) plan, often referred to as a "Mirror Plan."

As the name suggests, a Mirror Plan is designed to sit right alongside your existing 401(k). It "mirrors" the features your employees already understand, investment choices, account statements, and tax-deferred growth, but it strips away the IRS-mandated contribution caps.

With a Mirror Plan, your executives can defer significantly more of their income, sometimes up to 50% or even 80% of their base salary and 100% of their bonuses, into a tax-deferred vehicle.

Why is this a game-changer for executive retention strategies?

- No IRS Limits: The "cap" is gone. Your executives can save what they actually need to save to maintain their standard of living.

- Tax Efficiency: Every dollar deferred is a dollar that isn't taxed today. It grows tax-deferred until retirement, often when the executive is in a lower tax bracket.

- The "Ownership Feel": By allowing key people to build a significant "bank" within the company, they start thinking like owners. Their future is tied to the company’s success.

The Power of Being Selective (Discriminatory)

One of the biggest headaches for any CEO or HR Director is the "all or nothing" rule of traditional benefits. If you want to give a 5% match to your rockstar VP, you usually have to give it to everyone in the company to pass IRS testing. That gets expensive fast.

A Mirror Plan is discriminatory. And in the world of executive benefits, "discriminatory" is a beautiful word.

It means you get to choose exactly who participates. Do you have a "Top 5" list of people who are indispensable to your five-year growth plan? You can build a Mirror Plan just for them. You don't have to include the entire staff. You can reward the people who carry the heaviest load without the massive overhead of a company-wide benefit increase.

The CFO’s Secret Weapon: Full Cost Recovery

Whenever I talk to a President or a CFO about adding a Mirror Plan, the first question is always: "What is this going to cost the company?"

The beauty of a properly structured NQDC plan through Schiff Executive Benefits is the Full Cost Recovery model. Unlike a traditional 401(k) where the company match is a "sunk cost" (it goes out the door and never comes back), a Mirror Plan can be informally funded using corporate-owned assets.

When structured correctly, the business can actually recover the cost of the benefits, the cost of the money, and even the administrative expenses over the long term. It transforms a "benefit expense" into a "strategic corporate asset."

Imagine being able to tell your board that you’ve secured your top three executives for the next ten years, and the long-term cost to the company is effectively zero. That isn't a pipe dream; it's high-level financial engineering.

Creating the "Golden Handcuffs"

In his book The 7 Habits of Highly Effective People, Stephen Covey talks about "beginning with the end in mind." When we design a Mirror Plan, we aren't just looking at tax savings today; we are looking at your exit strategy or your succession plan ten years from now.

By using a Mirror Plan, you can implement vesting schedules that act as "golden handcuffs." If a competitor tries to poach your CTO, that CTO has to look at their Mirror Plan balance, which might be hundreds of thousands of dollars in tax-deferred wealth, and realize they lose a significant portion if they walk away before a certain date.

It changes the conversation from "How much is the other guy offering?" to "Can I afford to leave this wealth behind?"

Why Most 401(k) Advisors Miss This

Most financial advisors are experts in "qualified" plans. They know 401(k)s, IRAs, and mutual funds inside and out. But nonqualified executive benefits require a different level of technical expertise. They require an understanding of IRS Section 409A, corporate tax law, and specialized funding mechanisms.

If your current advisor hasn't mentioned a Mirror Plan to you, it’s likely because they aren't equipped to build one. They are trying to solve a 21st-century retention problem with a 20th-century toolbox.

At Schiff Executive Benefits, we don't just "sell plans." We consult. We look at the trajectory of your business, the tax burden of your top earners, and the competitive landscape of your industry. We help you build a moat around your best people.

Is a Mirror Plan Right for You?

Ask yourself these three questions:

- Are your top-paid employees complaining (or quietly frustrated) about the 401(k) limits?

- Is your business currently "failing" its 401(k) non-discrimination tests, resulting in refunds to your high-earners?

- Would your business suffer a major setback if your top three key employees left for a competitor tomorrow?

If you answered "yes" to any of those, it's time to look beyond the standard benefit package. The world is becoming more uncertain, and the competition for talent is only getting fiercer. You can't afford to be average when it comes to rewarding your best people.

Your Next Step

Building a world-class executive team is hard. Keeping them shouldn't be.

If you’re ready to move past the IRS caps and start rewarding your "vital few" with a plan that actually reflects their value, let’s talk. We aren't here to give you a sales pitch; we’re here to show you a blueprint.

Sit back, grab your coffee, and take a look at our process. We’ve spent decades helping companies like yours realize their dream value by securing the people who make that value possible.

Let’s build something that lasts. Let’s build your Perfect Plan®.

Ready to explore a Mirror Plan for your team? Contact us today for a confidential consultation.

Ready to talk?

If you're wondering whether a Mirror Plan could help you attract, retain, and reward your key people more effectively, let's have a conversation.