title: "The 5 'What Ifs' That Keep Business Owners Awake at Night"

meta_title: "The 5 What Ifs for Business Owners | Schiff Executive Benefits"

description: "The 5 What Ifs every business owner should address: succession, buy/sell planning, executive retention strategies, COLI funding, and retirement income certainty."

meta_description: "The 5 What Ifs every business owner should address: succession, buy/sell planning, executive retention strategies, COLI funding, and retirement income certainty."

keywords:

- executive retention strategies

- business succession planning

- buy sell agreement funding

- COLI

- deferred compensation

- retirement income planning

"Success is a lousy teacher; it seduces smart people into thinking they can't lose." This observation, often attributed to Bill Gates, captures the precarious nature of business ownership. You have spent years, perhaps decades, building an engine of growth. You have weathered economic cycles, navigated hiring crises, and outmaneuvered competitors. Yet, in the quiet hours of the night, when the emails stop and the house is still, a different kind of tension takes hold. It isn't the tension of what happened today, but the anxiety of what could happen tomorrow.

At Schiff Executive Benefits, we believe that the foundation of any great enterprise isn't just its current balance sheet: it’s the strength of its contingencies. We call these the "What Ifs." Our mission is simple: Helping Business Owners, Executives, and their families plan for all of life’s "What Ifs."

By addressing these five core scenarios, we focus on Restoring Alignment and Retention, ensuring that your legacy is protected and your future is guaranteed.

Quick next step: Start your own Business Valuation here: https://schiffbenefits.com/articles-and-forms/business-valuation/

1. What if you ended up in business with your partner’s widow or widower?

It is an uncomfortable thought, but a necessary one. Most business partnerships are built on a foundation of mutual skill and shared vision. You and your partner "click." But what happens if that partner passes away unexpectedly? Without a robust, funded buy/sell agreement, their shares of the company typically pass to their heirs.

Suddenly, your new 50% business partner might be a grieving spouse who has never stepped foot in your warehouse or attended a board meeting. They may want to be involved in operations they don't understand, or more likely, they may demand dividend distributions to replace the deceased partner's income: distributions the company might not be able to afford while trying to replace a key leader.

Effective business succession isn’t just a legal document in a drawer; it is a financial strategy. Are you using Split Dollar Life Insurance to fund the buyout? Does your agreement have a clear valuation formula that prevents a legal battle during an already emotional time?

2. What if someone came to you today and said they wanted to buy your business?

Every owner has a "number": that figure that would make all the years of sacrifice worth it. But an unexpected buyout offer is a double-edged sword. If an offer arrived tomorrow, would your business be "exit-ready"?

Potential buyers don't just look at your EBITDA; they look at the stability of your leadership team. If the value of your company is entirely tied to you, the buyer will likely discount the price or insist on a long, grueling earn-out period. To realize your dream value, you need to prove that the business can thrive without you.

This is where exit strategies and incentives like Phantom Stock come into play. By giving your key executives a "stake in the outcome" without giving away actual voting equity, you align their interests with yours. When a buyer sees a motivated management team with "Golden Handcuffs" in place, your valuation skyrockets. You move from selling a job to selling a high-performing machine.

Want to pressure-test what your business is worth before an unsolicited offer lands on your desk? Start here: https://schiffbenefits.com/articles-and-forms/business-valuation/

3. What if your top salesperson or manager left for any reason?

Imagine your top revenue generator walks into your office on a Monday morning and hands you a resignation letter. They aren’t just leaving; they are heading to a competitor for a 20% raise and a "better" benefits package.

The cost of losing a key executive is often calculated at 200% to 300% of their annual salary when you factor in lost momentum, recruitment costs, and the "brain drain" of institutional knowledge. In today’s talent-starved market, standard 401(k) plans and basic health insurance are no longer enough to win the war for talent.

To keep your "MVPs," you need executive retention strategies that actually resonate. We specialize in Non-Qualified Deferred Compensation (NQDC) and Executive Bonus Plans that create a powerful incentive for leaders to stay. We ask the hard question: What is the cost of doing nothing? If you aren't providing a Perfect Plan® for their future, your competitor will.

4. What if you could incent senior execs to retire while also retaining their replacement cost-efficiently?

There comes a point in every organization’s lifecycle where a transition is necessary. You have a loyal, senior executive who has been with you for twenty years. They are ready to slow down, but the cost of funding their retirement "promise" while simultaneously paying a high salary to recruit their successor can put a massive strain on company cash flow.

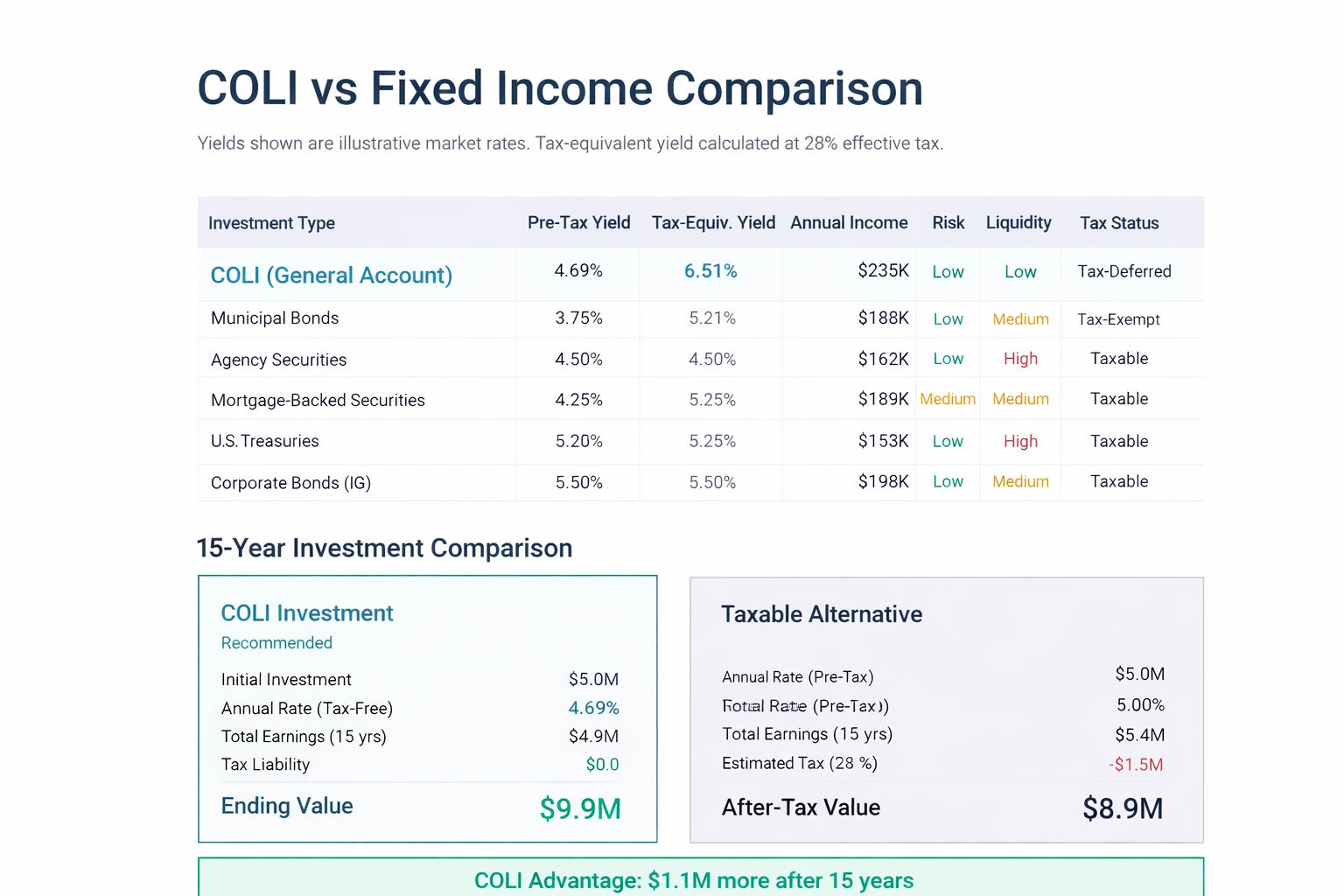

This is a common friction point in corporate and bank leadership. The solution lies in Corporate Owned Life Insurance (COLI). This is not just an insurance policy; it is a sophisticated financial asset that can provide tax-deferred growth to help offset the liabilities of executive benefits.

As shown in the chart above, strategies like COLI can significantly outperform traditional fixed-income investments, providing the liquidity and yield necessary to fund retirement obligations without depleting the company’s operating capital. It allows the senior executive to retire with dignity while giving the company the financial "breathing room" to hire the next generation of leadership. You can learn more about how we structure these for corporations on our COLI information page.

5. Lastly, when I retire, what if I run out of money?

This is the ultimate "What If." You have spent your life managing risk for your company, your employees, and your customers. But who is managing the risk for you?

Many high-net-worth business owners are surprised to find that their standard of living in retirement requires a cash flow that their traditional investments might not guarantee, especially in a volatile market or a high-tax environment. The fear isn't just about "having enough"; it's about the "sequence of returns" and the impact of taxes on your distributions.

This is why we developed The Perfect Plan®.

The Perfect Plan® is designed to provide a fixed rate and a fixed flow of income, removing the guesswork from your post-career life. It is about moving from "accumulation" to "distribution" with absolute certainty. We focus on tax-efficient strategies that ensure your wealth lasts as long as you do, protecting your family’s lifestyle and your professional legacy.

Moving from Anxiety to Authority

These five questions are not meant to cause alarm; they are meant to spark action. In the world of executive benefits, silence is the greatest risk. The longer you wait to address these "What Ifs," the fewer options you have when the crisis finally hits.

Are you ready to stop reacting to the market and start leading your legacy?

At Schiff Executive Benefits, we don't just sell products; we architect security. We work alongside your existing team of advisors: your CPAs and attorneys: to ensure that every piece of your financial puzzle fits together. Whether you are a corporation looking to optimize your COLI strategy or a private business owner looking to secure your family's future, we are here to guide you through the "unstable" and into the "guaranteed."

Succession, retention, and retirement are not separate silos; they are the three pillars of a healthy business. When they are aligned, you sleep better. When they are funded, you lead better. If you are evaluating broader executive retention strategies, the right structure can help you attract, retain, and reward key people without forcing a one-size-fits-all approach.

Sit back, grab your coffee, and let’s start a conversation.

You’ve built something incredible. Now, let’s make sure it’s built to last. Come join us at Schiff Executive Benefits and discover how we can help you plan for all of life's "What Ifs."

To dive deeper into these strategies, listen to our latest episodes on The Perfect Plan® Podcast, where we break down the technicalities of 409A compliance, exit planning, and the macro-economic trends affecting business owners today.

Additional resources (go deeper, stay in one place):

- Start your Business Valuation (first step): Get a baseline before you negotiate, gift, sell, or recruit your next key leader: https://schiffbenefits.com/articles-and-forms/business-valuation/

- The Business Owner’s Dilemma (Ali Nasser): Listen/watch the episode on our channel here (podcast hub with the embedded player): https://schiffbenefits.com/posts

- Dan Zugell on ESOPs: Explore the SEB hub page (embedded podcast + links out to the YouTube conversation): https://schiffbenefits.com/posts

Ready to address your "What Ifs"? Contact us today for a confidential consultation.

Ready to talk?

If you’re thinking about deferred compensation, executive retention, or how to structure a plan that fits your goals, let’s talk it through.